Previous Post

Sovereign Data Center Security: Essential Dos and Don'ts for Your Organization

.webp)

.svg)

Taiwan's AI data center market is drawing a new class of local entrants from construction, solar development, and property, at the same time as government policy limits grid power and rewards efficiency. This article describes who is entering, the 2 operating models available to them, and the criteria that indicate which partners are building for the long term.

Taiwan's earlier data center buildouts were carried by large established operators. The current wave looks different. Local companies are entering from construction, solar development, and property, and some may be willing to own GPUs and add compute services to the real estate they hold.

The pull is public policy as much as demand. The government's AI New Ten Major Infrastructure Projects program plans roughly NT$200 billion (about US$6 billion) of investment through 2028 and aims to place Taiwan among the top 5 countries in computing power. More than NT$30 billion (about US$950 million) was earmarked in the 2026 central budget as first-year funding, although the budget was still awaiting legislative approval as of late April 2026, so the first-year money had not yet been released.

Flagship private projects are scaling alongside it, including a Foxconn and NVIDIA facility in Kaohsiung, in southern Taiwan, expected to reach 100 MW at full capacity. That combination of policy money and visible projects is why companies holding land, power relationships, or capital now treat data centers as an adjacent business they can enter.

The first filter on any entrant is power. Taipower, the state-owned utility, has restricted new electricity applications from data centers above 5 MW in the north of the island (north of Taoyuan, the region that includes Taipei) unless new generation capacity is built. The Ministry of Economic Affairs has enforced a ceiling of 1.5 on PUE, the ratio of a facility's total power draw to the power that reaches its computing equipment, for hyperscale sites since November 2025, and tiered tariffs introduced in January 2026 add surcharges of up to 20% for inefficient facilities, while compliant operators receive fast-track permits and rate discounts.

The supply side explains the restrictions. Taiwan imports close to all of its primary energy and is part-way through a long-planned shift in its generation mix, with new gas, solar, and wind capacity being added and the role of nuclear generation under active review. Against demand that is rising quickly from AI and semiconductor manufacturing, large new loads compete for grid capacity that is still being built, which is why the utility now screens where and how much new data center load it will connect.

This is the context in which some Taiwan capital pairs with foreign power and property positions, where power can be easier to secure. It is also the reason the first question about any announced project is where its power allocation stands, because a project's secured power says more about its viability than its announced GPU count.

Once a site has power, the business divides into 2 models. The first builds the facility and leases space and power to tenants, so revenue is property-shaped and the capital sits mostly in construction. The second buys GPUs and sells compute directly, the way a cloud does, which makes the capital requirement much larger and renews it with each hardware generation, because the value of the asset sits in the chips rather than the building. Financing separates the 2 in practice.

Secondary trading in datacenter GPUs runs through brokers rather than an open exchange, so there is no published price history a commercial bank can use to value the chips as collateral or to model recovery in a default. Most GPU purchases are therefore funded from the buyer's own cash.

Lending against GPUs does exist, but it sits with private credit funds rather than banks. CoreWeave secured a $2.3 billion GPU-backed facility in 2023 and a further $7.5 billion in 2024, and Lambda closed a $500 million GPU-backed securitization in 2024, with firms including BlackRock and Carlyle among the lenders. Lenders in that market still treat the economic shelf life of the chips as the open risk.

The practical effect in Taiwan is that the operate-compute model stays open mainly to companies that can fund hardware from their own balance sheet. That keeps most new entrants on the build-and-lease side, or in partnership structures where one party brings the site and capital and another brings the compute operation.

Among the land buyers, intent varies. Some bought to develop and operate over years. Others bought to resell once surrounding values moved. Both are ordinary property strategies, but only the first supports a compute partnership, because an AI data center pays back over multiple hardware and contract cycles rather than over a single land transaction.

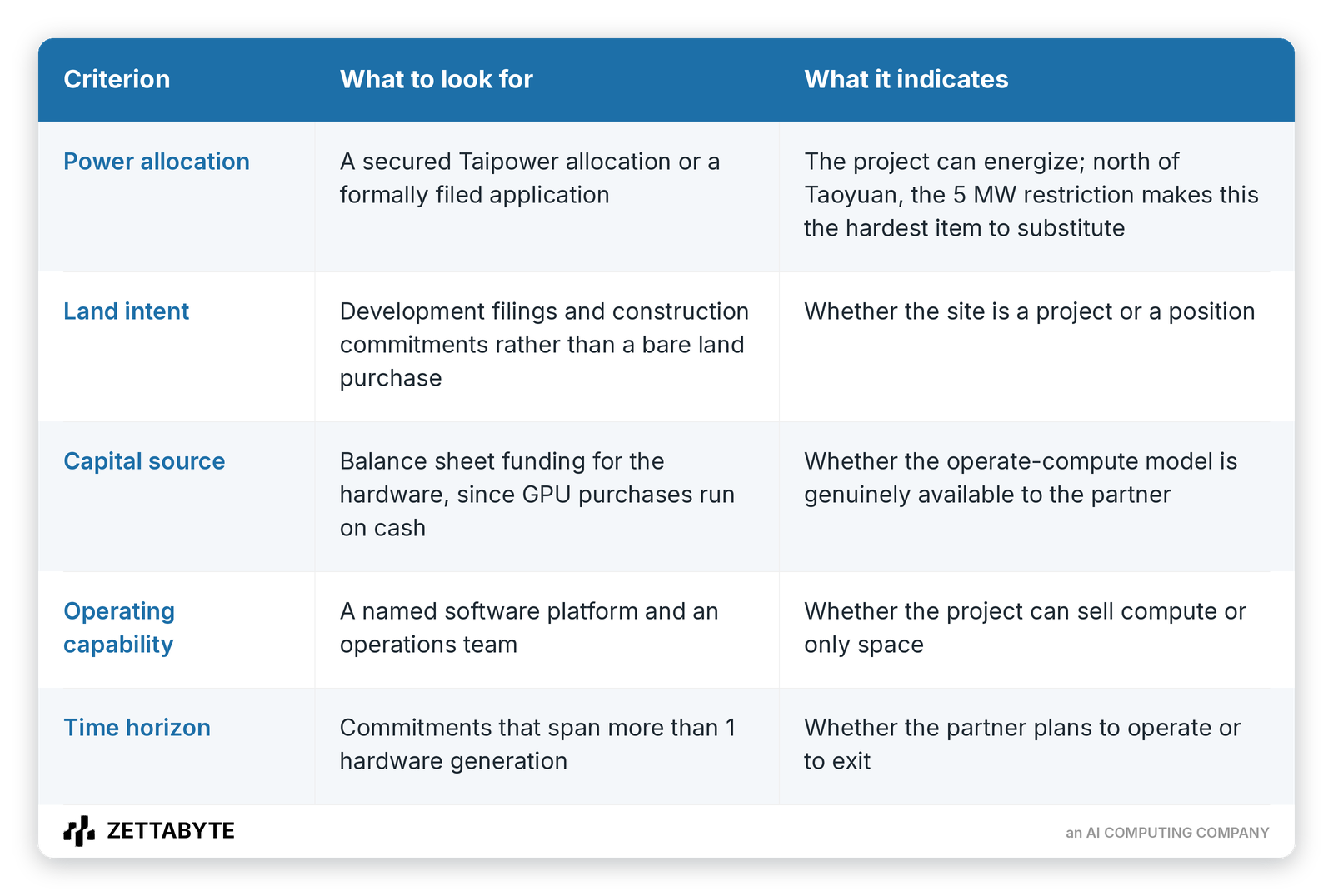

The horizon is usually readable from public facts before any negotiation starts:

A separate group of entrants arrives with capital and hardware supply but without the capability to run a cloud. Operating compute at scale means scheduling and sharing the cluster across tenants, metering and billing usage, and keeping utilization high through failures and maintenance. The hardware purchase does not include that capability.

An entrant in that position has 2 realistic paths. It can lease space and power and stay out of the compute business, which returns it to the first model. Or it can partner for the operating layer, contributing the site, the capital, and the supply relationships while the partner contributes the software platform and the run capability. In the partnership discussions we see locally, the second path is the more common shape, because it lets each side grow with the asset rather than one side carrying all of the capability risk.

The operating-layer partner role described above is the one Zettabyte fills. zSUITE, the company's sovereign AI compute platform, supplies the software a site owner needs to run purchased GPUs as a cloud: multi-tenant governance with role-based access, metering, and billing; orchestration and topology-aware scheduling across the cluster; and monitoring with fault recovery to hold utilization through failures and maintenance. The platform runs heterogeneous hardware without tying the operator to a single vendor.

In a partnership, that divides the work along the lines each side can carry. The partner contributes the site, the secured power, the capital for hardware, and local supply relationships. Zettabyte contributes the platform and the capability to operate the cluster, through a private deployment, a license subscription, or a turnkey build, depending on how much of the stack the partner wants to own. The arrangement lets a construction, solar, or property entrant enter the operate-compute model without first building a cloud operations team, and it lets each side grow with the asset rather than one side carrying the full capability risk.

Taiwan's policy program will keep drawing entrants, and which of them get built will continue to depend on power availability. For anyone weighing a partnership, the useful information is already public: where the power stands, what the land filings say, whose cash funds the hardware, and who runs the software.

The criteria condense into a short checklist, and each one is observable before a term sheet.